I've been working on the Commons proposal — the idea that Seattle Center should run the Arch building as a year-round public commons while the SCC keeps the Summit for conventions. To make the case, I needed to understand the convention center's finances.

The audited financials tell a story that's been covered: a $69.4 million operating loss, $25 million in reserves, a CEO who uses the word "fragile." The organization loses money on operations — it earns $58.6 million running two buildings but spends $75 million. The gap is plugged by lodging tax revenue, which also services $1.9 billion in bonds.

That was concerning enough. Then this week I pulled the actual bond documents off EMMA and read the debt service tables.

Balloon Approaching

In bond finance, a "balloon payment" is a large lump-sum principal payment that comes due after a period of smaller regular payments — like a mortgage where you pay mostly interest for years, then suddenly owe a massive chunk of principal all at once. Balloon payments are how borrowers keep their near-term costs low. They're also how crises get deferred.

The convention center's bonds require about $85 million per year in debt service — interest plus principal. Seattle's lodging tax (7% on hotel rooms) produced $99.9 million in 2024. King County's extended rate (2.8%) added another $6.4 million. Total: roughly $106 million to cover $85 million in bond payments, plus the convention center is losing $16.4 million a year on operations.

That's tight. Combined with King County's 2.8% rate, total lodging tax is roughly $106 million — leaving about $5 million in buffer after debt service and the operating shortfall. A recession, a shift in where convention attendees sleep — any of these could erase that margin.

But I figured the debt service was a known quantity. Everybody involved — the board, the bondholders, the rating agencies — presumably understood the payment schedule. So I downloaded the bond official statements from EMMA and read the debt service tables.

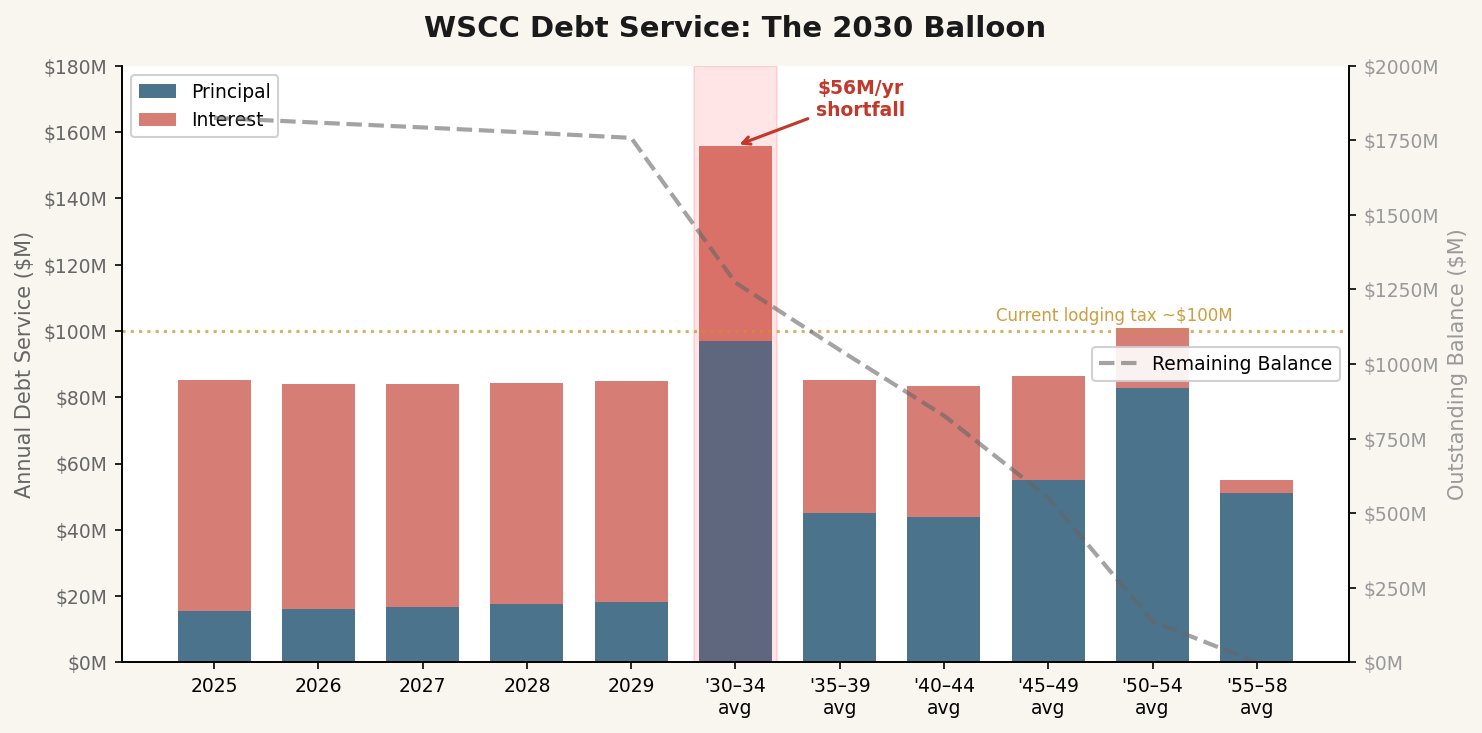

Starting in 2030, the balloon inflates. Debt service doesn't stay at $85 million. It nearly doubles.

The WSCC PFD's own 2024 audited financial statements (Note 6, page 29) show the scheduled requirements:

- 2025–2029: ~$85 million/year

- 2030–2034: ~$156 million/year — $779 million over five years

- 2035–2039: ~$85 million/year (back down)

That spike is the balloon — mandatory sinking fund redemptions on the term bonds that financed the Summit's $1.9 billion construction. The bonds were structured to keep payments low in the early years and concentrate principal repayment into 2030–2034. At current lodging tax levels, that's a $56 million annual shortfall. Every year. For five years.

And the state backstop — Washington's guarantee that covers any shortfall in debt service — expires in 2029. One year before the balloon arrives.

What the Bond Underwriters Promised Investors

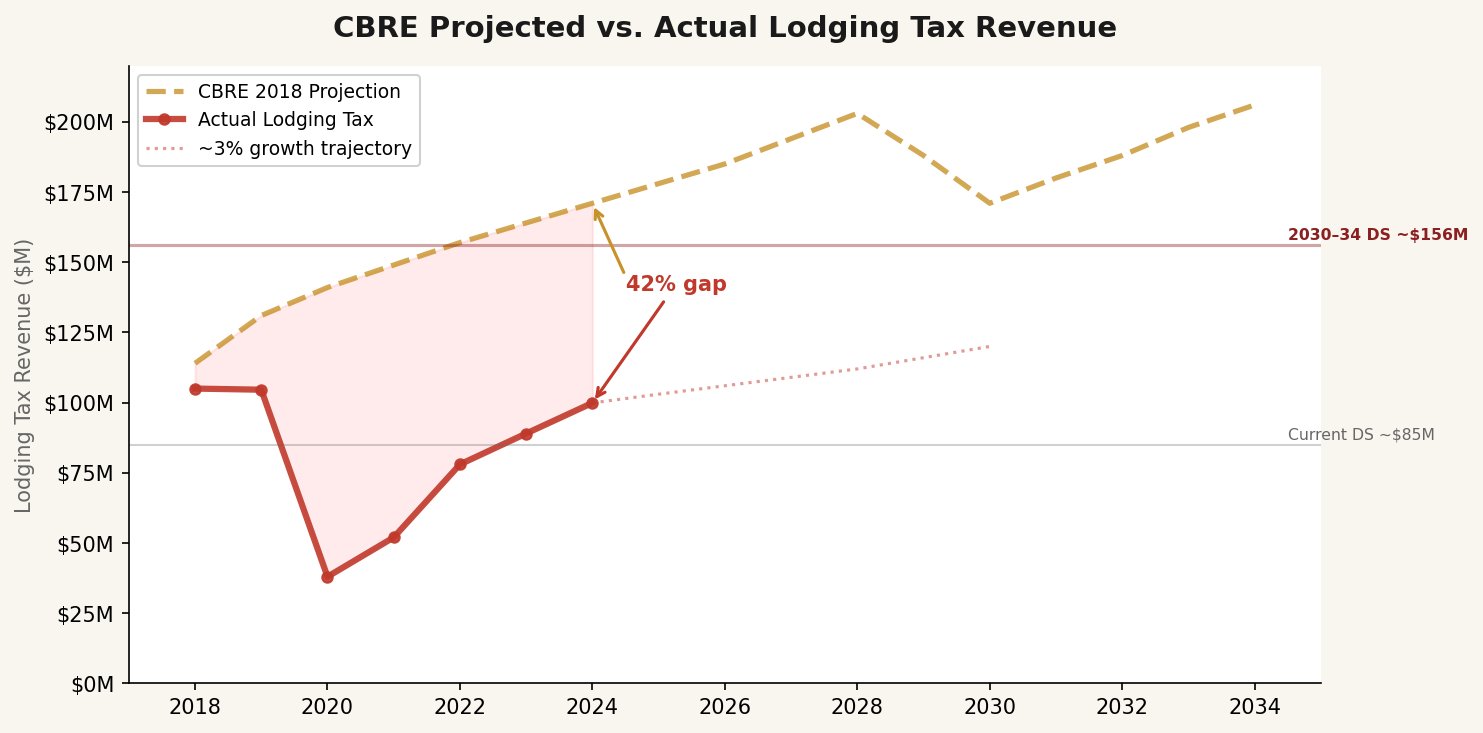

When the 2018 bonds were issued to finance the Summit, the underwriters — Citigroup, Goldman Sachs, RBC, BofA Merrill Lynch, and J.P. Morgan — hired CBRE Hotels Advisory, one of the largest commercial real estate advisory firms in the world, to produce a 30-year forecast of lodging tax revenues. That forecast (Table I-1, page 141 of the official statement) was the basis on which investors bought over $1 billion in bonds.

Here's what CBRE projected versus what actually happened:

| Year | CBRE Projected | Actual | Gap |

|---|---|---|---|

| 2018 | $114M | $105M | −8% |

| 2020 | $141M | ~$38M | −73% |

| 2024 | $171M | $99.9M | −42% |

| 2028 | $203M | ? | ? |

| 2030–34 avg | ~$190M | ~$106M trajectory | −44% |

In 2018, CBRE assumed an average 3% annual ADR growth with variations for anticipated supply/demand cycles (including a projected pullback around 2029–2030 as new hotel supply absorbed demand), 80% occupancy, and 2% supply growth — compounding over 30 years. They assumed the Summit would open in mid-2021. They projected lodging tax would blow past $200 million by the late 2020s.

None of that happened. COVID broke the baseline. Bellevue emerged as real hotel competition. Remote work permanently reduced business travel. The Summit opened 18 months late at $300 million over budget.

The debt service spike in 2030–2034 was structured to be covered by lodging tax collections in the $170–200 million range. Even at $106 million combined, the math doesn't work.

Five Years Later, the Masks Are Off

In 2021, the District refinanced $544 million in bonds. The official statement is candid about how much uncertainty existed:

"The District has not contracted for an updated forecast of Lodging Tax Revenues in connection with the issuance of the 2021 Bonds."

"There can be no assurance regarding the timing and strength of any recovery."

That was fair in 2021. Nobody knew what post-COVID recovery would look like. Refinancing at lower rates was the right call.

But the document also included this projection:

"The District projects that Lodging Tax Revenues will recover to provide more than 1x debt service coverage on outstanding obligations in 2023 and to 2019 levels by 2024."

It's now 2026. We have the answer. Lodging tax did not reach 2019 levels by 2024. The $99.9 million collected was below the 2017 level of $104.6 million. The CBRE forecast that underpinned the original bonds is running 42% behind. And the debt service schedule that was structured around $170–200 million in annual lodging tax is four years away from its peak.

That's not a criticism of the 2021 decision. It's a question about the 2026 silence. The data is in. The gap is clear. Why isn't this the headline?

Well — now it is.

What Happened to Other Cities

I looked for precedents — other convention centers or public facilities that hit a debt service wall. The pattern is remarkably consistent.

McCormick Place, Chicago. The closest parallel to Seattle. Tourism tax-backed bonds with a state backstop mechanism. COVID drove monthly collections down 78%. The authority drew $15 million directly from the state backstop. Fitch downgraded the bonds to BB+ — junk. Between 2010 and 2021, the authority restructured its debt seven times. One difference: Chicago's state backstop does not have an expiration date.

KFC Yum! Center, Louisville. Revenue fell short of projections. Moody's rated the arena bonds Ba3 — junk. To avoid default, the authority issued $389 million in refunding bonds, but only after securing strengthened guarantees from the state of Kentucky, Louisville Metro Government, and the University of Louisville. A top state official said default "would be unacceptable." Final maturity was extended five years.

Rupp Arena, Lexington, KY. COVID caused a 90% revenue decline on $275 million in convention center debt. The authority couldn't make $8 million in bond payments. The city used a "scoop and toss" refinancing — rolling near-term debt into the future — backed by the city's own general obligation credit.

San Antonio Grand Hyatt. Convention center hotel bonds. Revenue and reserves were completely depleted. The city paid $10.4 million in hotel occupancy tax to cover the shortfall. The hotel was ultimately sold to an out-of-state nonprofit to settle the debt.

Every case shares a thread: the original revenue projections were too optimistic, the crisis arrived faster than expected, and the restructuring was more expensive for having been delayed.

No precedent I found combines all four of the WSCC's risk factors: a 42% revenue projection miss, a debt service spike from $85M to $156M, a state backstop expiring immediately before the spike, and current revenue already insufficient to cover the approaching peak.

Can They Grow Their Way Out?

To cover $156 million/year in debt service from lodging tax alone, Seattle would need roughly $2.2 billion in annual taxable hotel revenue. That's a 65% increase over the ~$1.34 billion implied by 2024 collections. Over six years — 2024 to 2030. A compound annual growth rate of about 9%, well above the best years Seattle has ever posted.

Seattle's taxable hotel revenue grew about 5–7% per year in the strongest pre-pandemic years. Even at 7% annual growth — an aggressive assumption sustained over six consecutive years — the city would reach roughly $2.0 billion by 2030. That produces about $141 million in lodging tax. Still $15 million short.

The sensitivity model on our financials page lets you test the numbers yourself. To hit $156 million in lodging tax, you need something like 28,000 hotel rooms at 78% occupancy at $290 ADR — all simultaneously, all sustained. Seattle currently has about 23,000 rooms at ~68% occupancy at ~$235 ADR.

Meanwhile, at Headquarters

Seattle Convention Center recently posted a VP of Commercial Strategy & Sales position through SearchWide Global, a national executive search firm. The posting describes "public sector stability" and "long-term commercial growth across both the Arch and Summit buildings." The longtime Director of Sales — at the organization since it opened in 1988 — transitioned to a Senior Advisor role.

The organization is hiring for growth. The bond documents suggest it cannot afford to operate both buildings through the 2030s at current revenue levels.

The Window

The math points to a bond restructuring. The question is when and from what position.

Before 2029, the state backstop is still in place. The credit ratings reflect the guarantee. Restructuring — extending maturities, modifying sinking fund schedules, right-sizing the operating footprint — can be negotiated from relative strength.

After 2029, the backstop is gone. After 2030, debt service has nearly doubled. Rating agencies will have repriced the credit without the state guarantee. Refinancing from weakness means higher rates, deeper concessions, fewer options. Every precedent shows the same lesson: restructure early or pay more later.

The 2018 bonds were structured for a world where Seattle's lodging tax would reach $200 million. That world didn't arrive. The debt service schedule doesn't care.

All figures from public documents: WSCC PFD 2024 Audited Financial Statements · 2018 Bond Official Statement (EMMA) · 2021 Refunding Bond Official Statement (EMMA) · CBRE Hotels Advisory, Forecast of Lodging Tax Revenues, July 18, 2018 · Interactive financial models at commons.conventioncityseattle.com/financials.

Ivan Schneider is the founding editor of the Convention City Dispatch. He lives on the Pike/Pine corridor.

Correction (March 17, 2026): An earlier version of this article stated that Seattle would need 12% annual hotel revenue growth "in four years" to cover the 2030 debt service spike. The base revenue figure ($1.34 billion) is from 2024 collections, making the correct timeframe six years (2024–2030) and the required CAGR about 9%. The 7%-growth scenario has been updated accordingly. The core finding — that current revenue trajectories cannot cover the 2030–2034 debt service spike — is unchanged.

Correction (March 25, 2026): An earlier version of this article stated total lodging tax revenue as "roughly $100 million." That figure ($99.9 million) is Seattle's 7% lodging tax alone. King County's extended 2.8% rate adds $6.4 million, for a combined total of roughly $106 million. The chart graphic uses the Seattle rate to match the CBRE forecast basis. The buffer estimate, trajectory comparison, and related text have been updated. The annual shortfall against the 2030–2034 balloon ($156 million/year) is $50 million at combined rates — still catastrophic, slightly less so than previously stated.